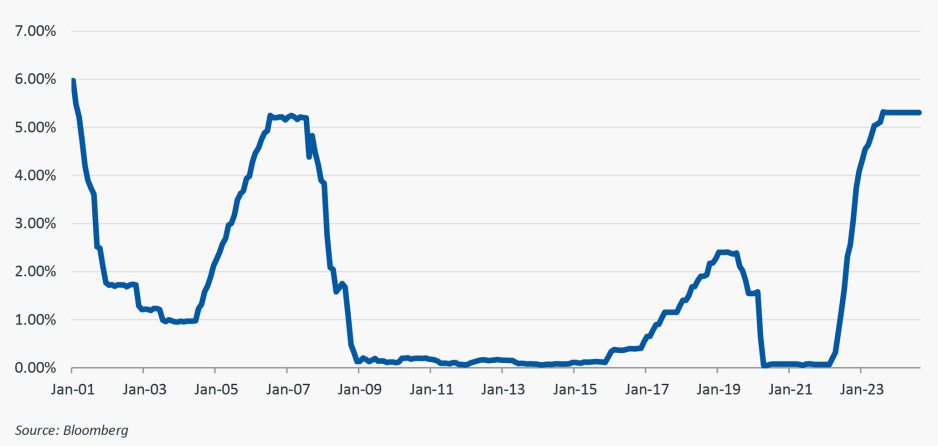

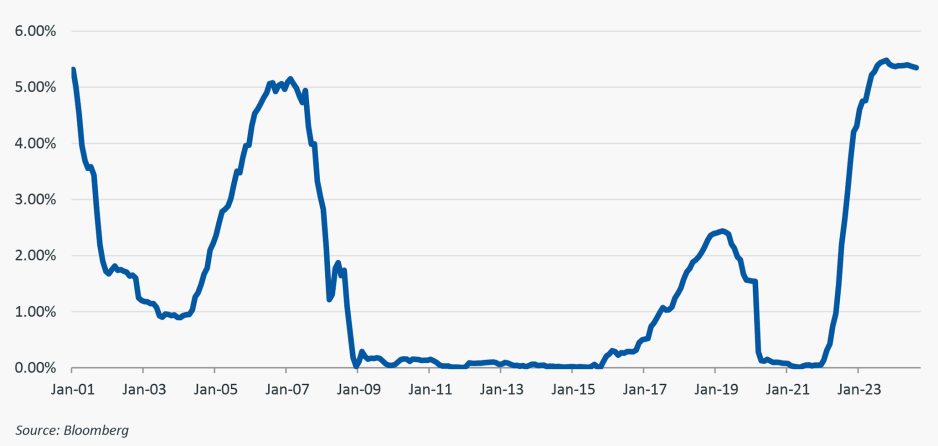

Short-term interest rates are at levels that have not been seen for almost 15 years. Beginning in 2022, and continuing into 2024, both the federal funds rate and the rate for 3-month Treasury bills have increased to approximately 5.33% as of early August (see Figures 1 and 2).

Figure 1: Historical Federal Fund Rates, January 2001-August 2024

Figure 2: Historical 3 Month T-Bill Rates, January 2001-August 2024

While the future direction of rates is always an unknown, there is growing consensus that short rates are likely to begin falling later this year. This is also expected to push the yield curve back towards its more historically normal, upward sloping shape—recent activity in the markets may signal that a bond market rally is already underway. Inflation continues to cool, and the unemployment rate has begun to inch up. Under the Federal Reserve’s dual mandate, it seeks to maintain both a robust job market and stable prices. As prices stabilize and signs of weakening in the job market begin to appear, the likelihood of a rate reduction increases.

This expected market dynamic creates a conundrum that has not been faced by fixed income investors in quite some time. When comparing rate expectations for different portfolio strategies, investors currently earn a lower rate for a longer duration portfolio than for a shorter duration portfolio. The resulting question that is asked frequently is, “Why shouldn’t I just maintain a shorter posture and reap the benefits of higher yield that the market is currently offering?”

The answer can be found in the reason for the current downward slope of the yield curve. In the simplest terms, the “inverted yield curve” represents investors’ expectations for lower rates in the future. If an investor stays in shorter-term securities (or funds), when those securities mature or are reinvested, it will likely be at lower rates as the market adjusts to Fed policy. By extending before rates begin to decline, it is possible to “lock in” higher rates for a longer period of time. Even though these longer rates might be lower than rates on the shortest maturities in the current rate environment, this strategy helps prolong the period when relatively higher rates are earned on the portfolio.

Generating earnings from cash assets

For years, organizations have grown used to earning practically 0% on cash assets. Because it has been so long since we have experienced a rate environment that provides for noticeable earnings, the art of generating excess earnings from cash assets may have gone dormant in the minds (and busy days) of treasurers. If so, it is time to bring that art back to life. No matter what narrative you believe about the direction of short-term rates, there is real money at stake if your organization is not taking advantage of the current rate environment with its available, liquid funds.

In a historically “normal” yield curve scenario, there have been two classic active management investment approaches to increase yield/investment returns above leaving assets in a government money market fund. These approaches have typically been:

- Purchase spread product (non-Treasury/Agency sectors)

- Extend in maturity

Spread products enhance returns because, based on the perceived lower relative credit quality, there is a requirement by investors to be compensated for the additional risk over the perceived safety of government debt. Similarly, investors have required additional yield to extend maturity out the curve due to the additional risk of the unknown path of rates over time (notwithstanding the current inverted yield curve).

Which option or combination of options an organization decides to pursue is a function of its liquidity needs and the types of funds it has available to invest. Active management of cash assets has historically employed analysis of the probability ascribed to an organization’s cash needs, balanced with an informed opinion on the likely direction of future rates to inform strategy and tactics. This probability analysis then sets the framework for investment options. Liquidity needs in the short and longer terms and probable interest rate directions drive the blend of investment targets. These range from highly liquid investments for more immediate, high-probability cash needs to investments that trade liquidity for rate enhancements.

However, by using the results of the above analysis, investors can take targeted advantage of either or both of these investment options and should be able to increase portfolio yields and long-term returns.

One category where the rate conundrum can be particularly vexing is in short-term, declining balance portfolios. These assets are typically associated with large capital projects, which often are paid out over a multi-year schedule. Investments can be tied to the draw schedule and targeted amounts can be invested to target longer maturities (draws) to lock in current rates and offer protection in the event that rates decline over the life of the project. While continuing to take advantage of the relatively high overall level of short-term rates, this approach helps ensure that project funds also contribute to cash generation for the organization until they must be spent.

Conclusion

The current interest rate environment has created opportunities for earnings from cash assets that have been largely unavailable for a generation of treasury managers. Investment options will be driven by the specific resources and needs of each organization, but all organizations have an opportunity to position their assets in a way that can help net significant, absolute earnings.

Investment involves risk, including loss of principal. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown. Products and services described herein may not be suitable for everyone. Carefully consider an investment’s objectives, risk factors, and charges and expenses before investing.

Information provided in this document is general in nature and should not be relied upon as investment advice specific to the reader’s investment objectives. Information is subject to change without notice. This information is not intended as a recommendation, offer or solicitation for the purchase or sale of any security or investment strategy nor does not consider a reader’s particular investment objectives, financial situations, or needs. KHIM, its affiliates, and financial advisors do not provide legal, tax, or accounting advice. You should consult your legal and/or tax advisors before making any financial decisions.

Any communication or information provided has been obtained from sources believed to be reliable at the time of publication, nonetheless, KHIM cannot guarantee, nor does KHIM make any representation or warranty as to their accuracy and you should not place any reliance on such communication or information. ALL INFORMATION, ANALYSIS AND CONCLUSIONS CONTAINED IN THIS DOCUMENT ARE PROVIDED “AS-IS/WHERE-IS” AND “WITH ALL FAULTS AND DEFECTS”. KHIM MAKES NO REPRESENTATION ABOUT THE SUITABILITY OF THE INFORMATION. UNDER NO CIRCUMSTANCES AND UNDER NO LEGAL THEORY SHALL KHIM BE LIABLE FOR ANY DAMAGES, WHETHER DIRECT, INDIRECT, INCIDENTAL, CONSEQUENTIAL OR SPECIAL ARISING FROM READER’S ACCESS TO OR USE OF THIS DOCUMENT.

Reading or utilizing information in this document or contacting or responding to our offices or registered investment advisers does not create an advisory relationship of any kind.

David Hiteshew, CFA, is a Senior Vice President, Portfolio Management, for Kaufman Hall's affiliate company, Kaufman Hall Investment Management.